The gold market is barreling towards an impending correction. An event that puts -millions- on the table for the taking.

All the signs are at plain sight. The S&P:TSX.V ratio is normally a consistent 0.8 to 1 – as seen below.

The Chart divides the S&P Index by The TSXV Index. As noted in the last mining bull market the index went from 0.7 to a high of 2.6. Today its around 0.2 after years of a prolonged slump. Can it get to previous levels… if so, serious upsiude for the sector.

The commodities bull run is going at a strong 2.5 to 2.6 ratio.

And, even so,

Mining stocks are sitting sit at a floor-level 1:0.02 ratio.

The sector has had a hard year at large.

However, nothing stays down forever.

We’re now entering correction territory. A sharp turn of the tide of mining vs. other stocks should be no surprise.

Fixing the foundations

The signs are not only in the numbers. An advocacy group conformed by the likes of Eric Sprott and Terry Lynch and the Canadian government are working on structural changes aimed to put a halt to predatory shorting in the mining sector. (Announcement expected by EOY; early 2021)

A major breather for the industry that would eliminate one of the negative factors that’s currently an inevitable part of investing in it, as well as accelerate its recovery. But, what rate of recovery are we looking at, if any?

A closer look at the rebound

Mining stocks have historically traded at a ratio of 1:1 or slightly higher when measured against comparable commodities.

Now? They’re barely trading at 35% of that.

They’ll have to triple in value just to get back to normal.

All these factors combine into an impending “tide to lift all boats” in the sector.

One of the best ways to leverage this unique landscape is aiming towards the microcap sector for maximum leverage.

Enter Chilean Metals Inc. (TSXV: CMX) – a microcap with an eye for state-of-the-art technology, a board with rock-solid, high-flying connections and multiple transnational projects.

Trading an unbelievable price.

The Chile-Canada Connection

Toronto’s Chilean Metals Inc. is an exploration company focused on the acquisition and development of mineral properties in Chile and Canada. It boasts a star-studded leadership and multiple exploration and development-stage projects.

The company is running a three-phase, three-location program consisting of two Chilean sites and a North American one.

In Chile: Project Zulema, located in Chile’s famed 3rd region – host of the Atacama mineral belt – Tierra de Oro, along the prolific Chilean iron oxide-copper-gold belt. In North America: CMX is working on the proposed acquisition of the BC-based Golden Ivan project.

CEO Terry Lynch said it best: “Exploration is risky. You must get good science before you begin drilling. You have to take quality risks, and sequence them. With each risk that’s taken successfully, you have to harness the momentum. Eventually you’ll get a win”.

A deeper dive

Tierra de Oro

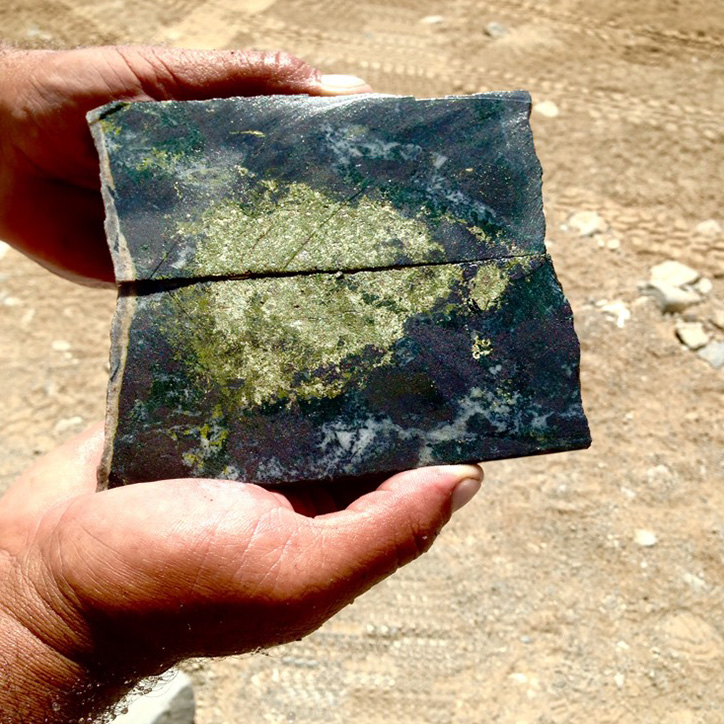

Chilean Metals’ wholly-owned Tierra de Oro-Chanchero (TDO) property is a part of Chile’s famed IOCG (iron oxide-copper-gold) belt. The belt hosts numerous copper-gold deposits including 3 megamines hosting 500 to a billion tons of resource. One of them, Candelaria, has reported reserves and production of 470 million tonnes at 0.95 % Cu, 0.22 g/t Au, 3.1 g/t Ag.

Aside from these larger projects, the IOCG belt hosts another half dozen smaller mines hosting anywhere from 50 to 100 tons of resource each.

The 14,000 acre location is in the vicinity of a city, highways, ports and a power grid – and the area’s climate allows for year-round exploration.

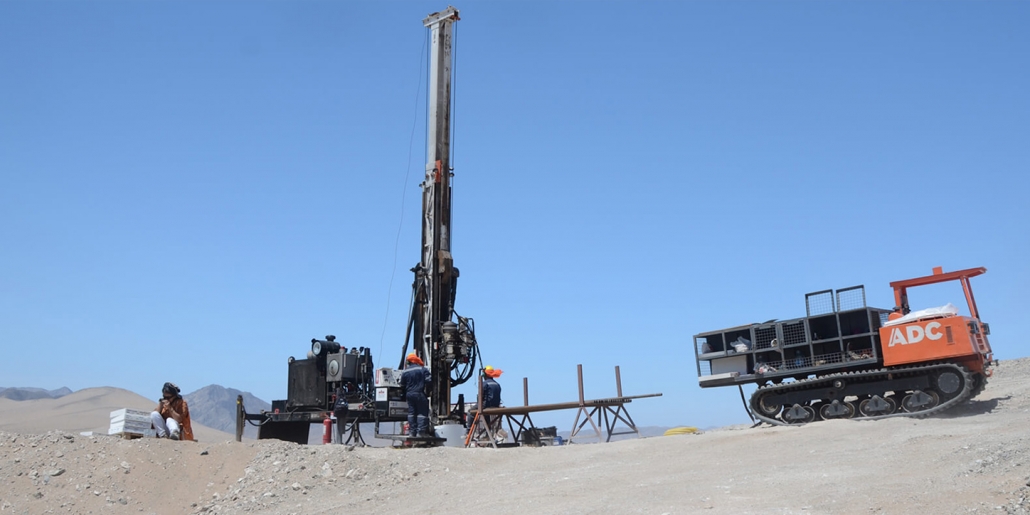

CMX has secured top AI firm Windfall Geotek to process all preexisting data and determine the most viable targets. Windfall has returned 4 ideal drill sites in the Chanchero IP zone of the property, which will all be drilled over December 2020.

If drilling is successful, all efforts turn to the project. If not, phase 2 begins.

Zulema

Similar in size to Tierra de Oro, the Zulema project borders Lundin Mining Corp.’s (TSXV: LUN.TO) Candelaria – a now-extinct megamine.

With their existing infrastructure and knowledge of the region, and after having hit bonanza-grade resource right next door, Lundin’s keeping a close eye on this project’s development.

So much so, that their senior mining expert’s interpretation of historical data has led CMX to put together additional geophysical testing.

A partnership with huge potential, blooms.

Golden Ivan

CMX’s Canadian project is right in the heart of the Golden Triangle – one of the most explosive exploration areas in the world.

The Golden Triangle has already produced 130 million ounces of gold, 800 million of silver and 40 billion of copper.

Extremely prospective. And CMX is right in the thick of the action, surrounded by some serious industry players.

Golden Ivans’ neighbors include Strikepoint at $30 million market cap – Scottie Resources at $45 million – and Ascot Resources at $350 million.

So, as it seems, investing in the Golden Triangle means dealing with some serious capitalization and high stock prices. Right?

Think again.

CMX’s current market cap is only $8 million.

A major discount from its neighboring comparables.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Into the books

There’s no way around it – CMX is astoundingly undervalued compared to its peers.

But how about the share structure? How much does management hold?

It’s solid. And they hold plenty.

Management and key shareholders: 40%

Board: 5%

To further strengthen the company’s financial backbone, 5 key brokers joined in for 5% each in the last round of financing. Another 20% under control.

And they’re expected to come back for more soon.

The final touch

The business model is clear – and Lynch laid it out perfectly:

“We’re using cool tech like AI to enhance our odds. We’re very well-connected in the mining space because of our mining leadership. All known players know me, trust me, that’s why I’m able to get attractive deals. I’m a square shooter. They know I’ll put the money on the ground and we’ll have a productive program to create value. That’s why I’m bullish now. I didn’t try to raise money in Chilean for years, but now I’m bullish. Now I’m gearing up to kick ass and take names”

Sound. But that’s not the end of it.

CMX has an ace up its sleeve –

The company recently finalized a development-stage deal in Québec. With it, they add an existing 43-101 resource of nickel and palladium to their asset portfolio.

It represents no exploration risk and could expand into a mine, making it worth anywhere from 50 to 100 million dollars.

Huge.

The jump from exploration only to development-stage company alone could catapult the stock price to CA$ 0.50 practically overnight and, if exploration targets are hit, much further north.

You have the primer. NOW is the time to make your move.

Add Chilean Metals to your portfolio soon.

ABOUT CHILEAN METALS

Chilean Metals Inc. (TSXV: CMX) is a Canadian Junior Exploration Company focusing on high potential Copper Gold prospects in Chile and Canada.

Chilean Metals Inc is 100% owner of five properties comprising over 50,000 acres strategically located in the prolific IOCG (“Iron oxide-copper-gold”) belt of northern Chile. It also owns a 3% NSR royalty interest on any future production from the Copaquire Cu-Mo deposit, recently sold to a subsidiary of Teck Resources Inc. (“Teck”). Under the terms of the sale agreement, Teck has the right to acquire one third of the 3% NSR for $3 million dollars at any time. The Copaquire property borders Teck’s producing Quebrada Blanca copper mine in Chile’s First Region.

In addition to its projects in Chile, CMX recently announced a proposed acquisition of the prospective early stage Golden Ivan project in the Golden Triangle, in British Columbia, Canada. The press release https://chileanmetals.com/wpcontent/uploads/2020/11/CMX_GoldenIvanAquisitionFinal.pdf describes this opportunity. The deal is subject to delivery to the TSXV of a Technical report on the project which is expected to be delivered in early January.